After a decade at the helm of the Bank of Japan (BOJ), the current governor Haruhiko Kuroda is stepping down. The choice of the new governor is of great concern to the market. This not only involves whether the quantitative easing policy implemented in Japan for many years will change but also the direction of the Japanese economy in the post-Abe era. According to Japanese media reports, Japanese government officials have approached BOJ Deputy Governor Masayoshi Amamiya, and have repeatedly discussed the possibility of him replacing Kuroda as the next governor of the central bank. From this point of view, the new BOJ governor candidate is surfacing.

According to media reports, most of the BOJ observers surveyed believe that the current deputy governor Amamiya is the most popular candidate, known for orchestrating the BOJ's early large-scale bond purchases and yield curve control (YCC). He served as Kuroda's right-hand man and advocated keeping an ultra-loose policy to get Japan out of deflation. Based on his previous work and attitude, if Amamiya takes office, this would be considered by the market as a possible continuation of Kuroda's policy. This has also caused a new round of depreciation of the yen and volatility in Japanese capital markets. In fact, researchers at ANBOUND have previously talked about how Japan's monetary policy may be the biggest uncertainty in 2023. With the gradual clarity of the BOJ's candidate, the likelihood of the central bank sticking to its super-loose policy has become greater. However, with inflation exceeding the target and international capital betting on a change in Japan's monetary policy, Japan now faces a huge dilemma. This also leads to the uncertainty facing the policy.

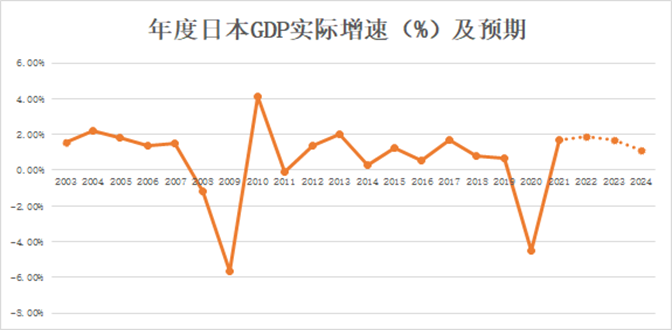

Figure: Annual Japanese GDP's Actual Growth Rate (%) and Expectations

Source: EasyBanking; chart plotted by ANBOUND.

The Japanese economy has achieved a growth rate not seen for many years despite the high inflation. However, with higher inflation and changes in the foreign trade situation, there is now a trend of slowing down. The increasing stickiness of inflation, which has brought about higher prices for imported products, has clearly affected the country's foreign trade and overall economic growth. The Japanese economy achieved 1.8% growth in the first three quarters of last year, but there was a contraction of 0.3% in the third quarter from a year earlier. The BOJ's forecasts in January have also all declined, with its expected GDP growth rate of 1.9% in the fiscal year 2022, previously expected to be 2.0%. It is expected that the GDP growth rate in the fiscal year 2023 will be 1.7%, previously expected to be 1.9%; and 1.1% in the fiscal year 2024, previously expected to be 1.5%. The Japanese government finalized its economic forecast for FY2023 at a cabinet meeting on January 23, with a real GDP growth rate of 1.5%. In contrast, the IMF expects it to grow by 1.8% in 2023. High corporate profits from the depreciation of the yen and the delayed effect of previous project implementation will also support Japanese companies' investments. However, in 2024, as the impact of stimulus measures disappears, its economic growth is expected to drop to 0.9%. In the post-Abe era, the effects of the super-loose policy pursued in Japan are waning. If inflation persists, the policy gap between Japan and the major economies will grow. For the BOJ, maintaining quantitative easing will further push the yen's depreciation and sustain inflation.

Previously, it had been reported in the media that the three main candidates for governor, whether those adhering to the super-loose policy like Amamiya or quantitative easing policy critic former BOJ deputy governor Yukio Yamaguchi, as well as the former deputy governor Hiroshi Nakasone are unwilling to assume the position. This reflects the dilemma facing the Japanese central bank's monetary policy. Last December, Japan's core CPI figure rose 4.0% year-on-year, exceeding the 2% target for many months in a row. If inflation is to be curbed, the BOJ's tightening of monetary policy is an inevitable move. Yet, if the policy shift is made, its implementation will be difficult and is likely to bring about a collapse in the Japanese government bond market, as happened when the BOJ relaxed the YCC ceiling last year.

After nearly 30 years of monetary easing, tightening monetary policy needs to address the risks associated with large swings in capital markets. Although market participants generally believe that the replacement of the BOJ governor is the right time for its monetary policy shift, any change in BOJ policy could trigger a sharp rise in the yen and long-term Japanese bond yields. JP Morgan expects that a policy shift in Japan could bring about a 4% to 5% appreciation of the yen, which would attract international capital back to Japan and exacerbate the global liquidity deficit. For China, South Korea, and Southeast Asian countries with close economic and trade ties to Japan, it will also bring exchange rate fluctuations, affecting the stability of local financial markets.

In fact, the yen has recently changed due to further clarity on the selection of a new governor. The yen, which had previously been in appreciation, has dropped. On February 6, the yen was down to around 132.50 at one point, a drop of about 0.7%, the lowest level since January 12. The offshore yuan fell more than 200 points against the U.S. dollar in early Asian markets, falling below 6.83, bringing the cumulative two-day drop to 900 points. The Korean won plunged 1.5% against the dollar at the opening. The dollar index also rose to a new three-week high of 103.24. This shows that the future trend of the Japanese central bank's monetary policy has a huge impact on emerging market countries, and the risk of uncertainty is still very significant in 2023. With the clarity of the BOJ governor's choice, the trend of its monetary policy has also become clear. That being said, there are still no definite answers to the questions if Japan's monetary policy will shift, when will it shift, and how it will shift. This will remain a black swan that plagues markets and related economies.

Final analysis conclusion:

As the future candidate of the Bank of Japan governor gradually becomes clear, the possibility of Japan continuing the super easing policy becomes more likely. However, inflation and growth have caused a dilemma that is still difficult to get rid of. Under internal and external pressure, the Japanese monetary policy is still facing the uncertainty of change.